Financials

CONDENSED INTERIM FINANCIAL STATEMENTS FOR THE SIX MONTHS AND FULL YEAR ENDED 31 DECEMBER 2025

Financials Archive![]() Note: Files are in Adobe (PDF) format.

Note: Files are in Adobe (PDF) format.

Please download the free Adobe Acrobat Reader to view these documents.

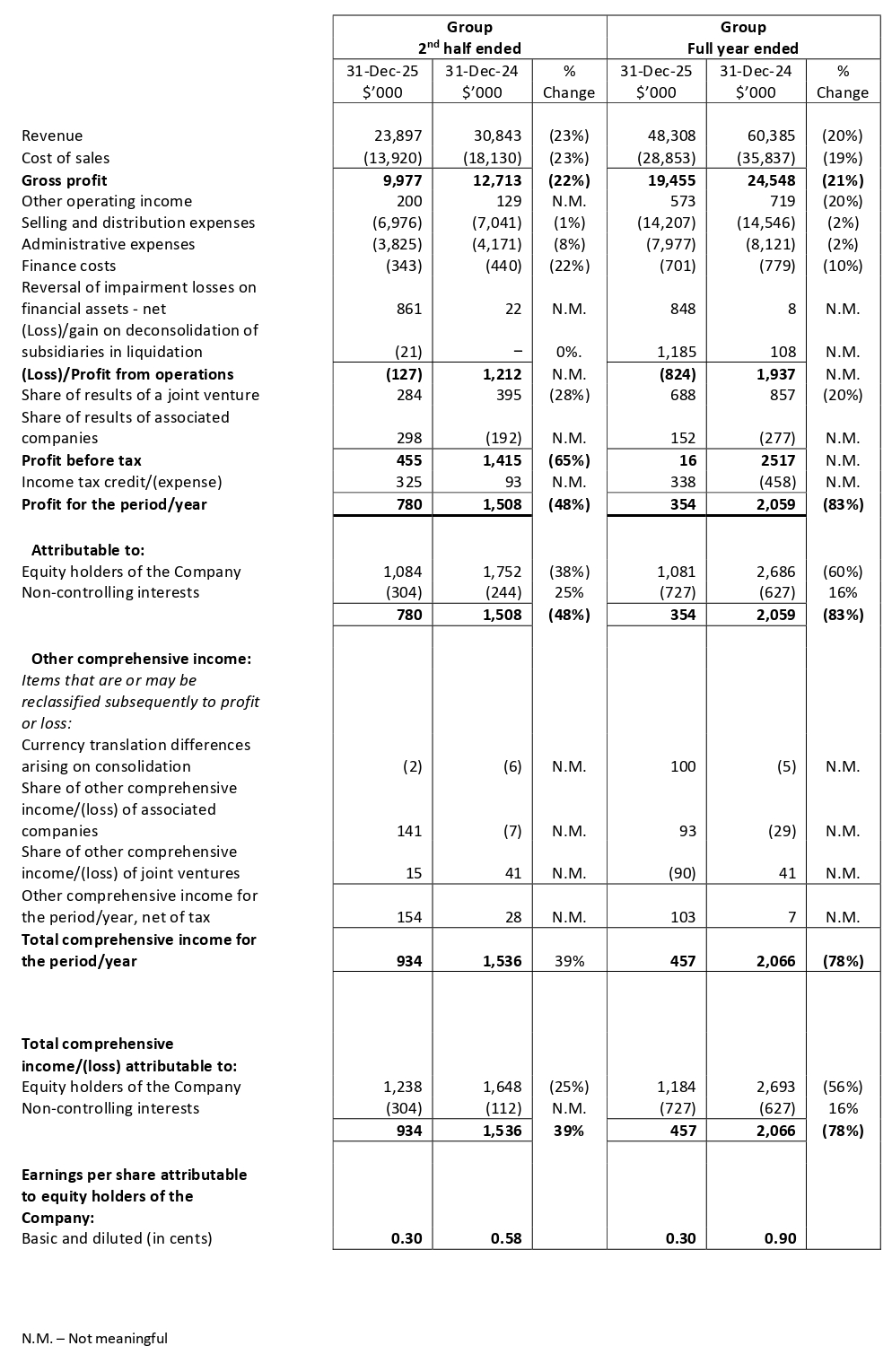

Condensed Interim Consolidated Statement Of Profit Or Loss And Other Comprehensive Income

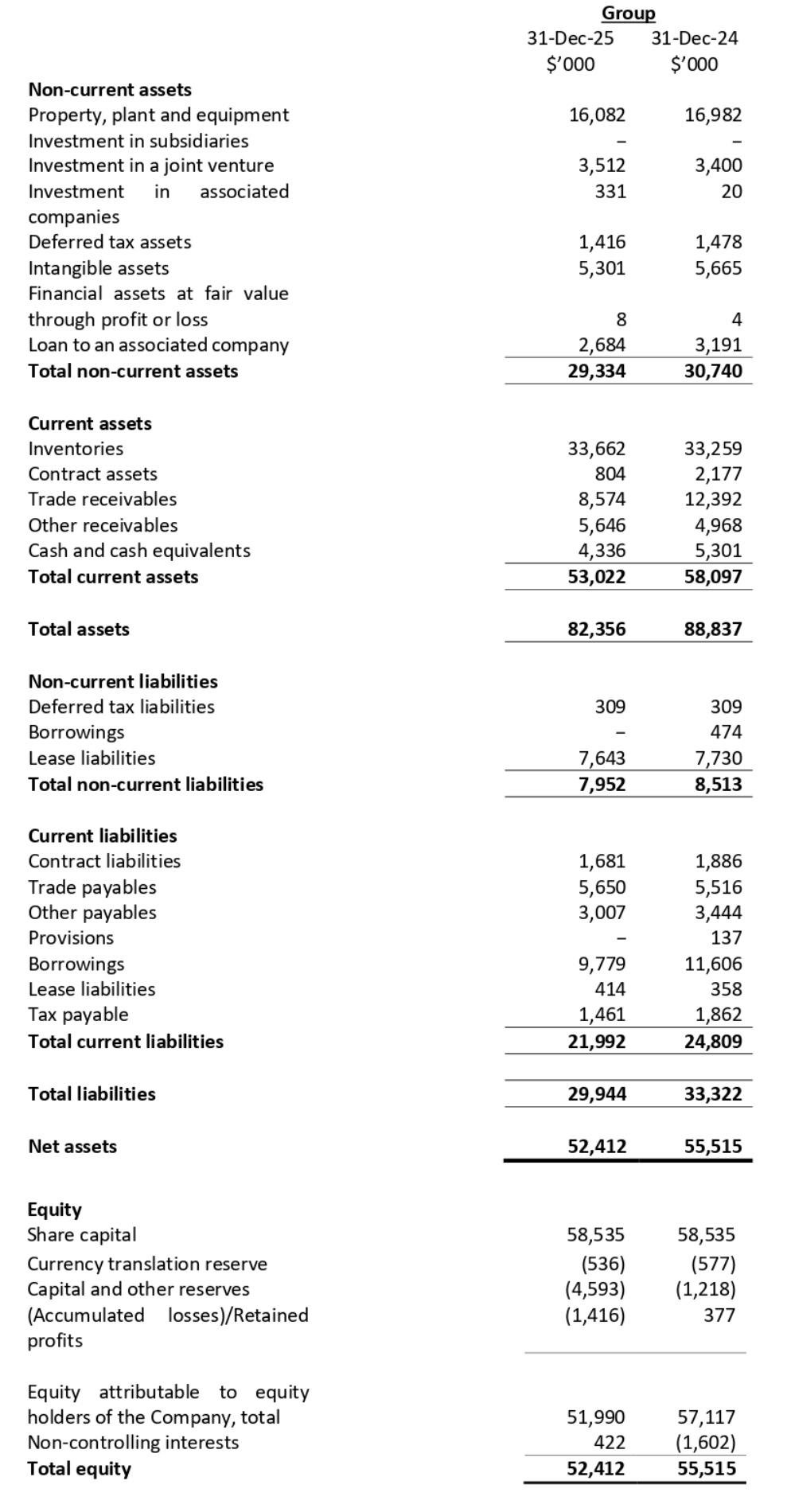

Condensed Interim Statements Of Financial Position

Review Of The Performance

Financial Performance of the Group

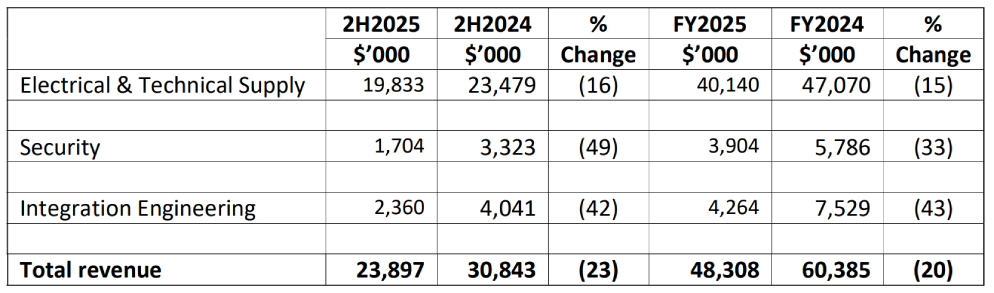

(i) Revenue

Electrical and Technical Supply

For 2H2025 and FY2025, revenue from the Electrical and Technical Supply Division decreased by 16% ($3.6 million) and 15% ($6.9 million) respectively mainly due to lesser revenue from shipyards.

Security

The Security Division comprises Infrared and Thermal Sensing Technology and Cyber Security businesses. Revenue from this division decreased by $1.6 million (49%) and $1.9 million (33%) for 2H2025 and FY2025 respectively due to lesser projects delivered and secured in both 2H2025 and FY2025.

Integration Engineering

For 2H2025 and FY2025, revenue for the Integration Engineering Division decreased by 42% ($1.7 million) and 43% ($3.3 million) respectively mainly due to lesser projects delivered and secured in both 2H2025 and FY2025.

(ii) Gross profit

The Group's 2H2025 gross profit margin of 42% is slightly higher than 2H2024 of 41%. However, 2H2025 gross profit decreased by $2.7 million from $12.7m in 2H2024 to $10.0 million in 2H2025, mainly due to lower revenue.

(iii) Other operating income/(expenses)

2H2025 recorded an other operating income of $0.2 million as compared to $0.1 million in 2H2024 mainly due to increase in government grants and sponsorship received.

(iv) Operating expenses

Selling and Distribution expenses remain comparatively unchanged.

Administrative expenses decreased by $0.4 million from $4.2 million in 2H2024 to $3.8 million in 2H2025 mainly due to:

- Decrease in personnel related cost. This is mainly due to higher writeback of bonus/commission as a result of lower revenue.

- Decrease in legal and professional fee.

- Decrease in equipment expenses due to reduction in infrastructure related cost (Microsoft and Office subscriptions) from the Security Division arising from a reduction in headcount.

Finance cost decreased by $0.1 million from $0.4 million in 2H2024 to $0.3 million in 2H2025 mainly due to decrease in interest rates and lower borrowings.

(v) Share of results of a joint venture

The decrease in 2H2025 share of profits of a joint venture was due to lesser profits from the Group's joint venture for 2H2025.

(vi) Share of results of associated companies

he Group recorded a share of profit of associated companies for 2H2025 as compared to a loss in 2H2024 due to better performance from associated companies.

(vii) Taxation

The increase in tax credit in 2H2025 was mainly due to recognition of deferred tax assets offset against tax expense during the year.

(viii) Net profit for the year

For FY2025, the Group registered a net profit of $0.4 million, compared to $2.1 million in FY2024 mainly due to lesser revenue.

Financial Position of the Group

Inventories

Inventories increased by $0.4 million from $33.3 million as at FY2024 to $33.7 million as at FY2025. This is mainly due to increase in Integrated Engineering division by $0.8 million and Electrical and Technical Supply division by $0.2 million. The increase is offset by a decrease in Security Division of $0.6 million.

Trade receivables

Trade receivables decreased by $3.8 million from $12.4 million as at FY2024 to $8.6 million as at FY2025. This is mainly due to decrease in Electrical and Technical Supply division by $2.3 million, Integration Engineering division by $1.2 million and Security division by $0.6 million as a result of lower revenue.

Borrowings

Total bank borrowings decreased by $2.3 million from $12.1 million as at FY2024 to $9.8 million as at FY2025 due to decrease in working capital loan of $1.2 million and repayment of term loan of $1.1 million.

Trade payables

Trade payables increased by $0.2 million from $5.5 million as at FY2024 to $5.7 million as at FY2025. This is mainly due to increase in payables from Electrical and Technical Supply division by $1 million offset against a decrease in Security division of $0.8 million.

Other payables

Other payables decreased by $0.4 million from $3.4 million as at FY2024 to $3 million as at FY2025 mainly due to lower accrual of bonus/commission of $0.4 million as compared to FY2024 as a result of lower revenue.

Cash flow review

The Group registered a higher net cash flow from operating activities of $4.6 million in FY2025 as compared to $0.8 million in FY2024. This was mainly due to decrease in inventories, contract assets and receivables. These were partially offset by reductions in contract liabilities and payables during the year.

The net cash flow used in investing activities decreased from $1.7 million in FY2024 to $0.6 million in FY2025 mainly due to lesser development cost incurred and loan repayment from an associated company.

The Group recorded a net cash used in financing activities of $4.9 million in FY2025 as compared to a net cash generated from financing activities of $1.0 million in FY2024 as a result of higher repayment of bank borrowings.

Commentary

Industry Trends and Competitive Conditions Relating to BH Global Corporation Ltd

Structural drivers such as regulatory compliance, fleet maintenance, energy security, and gradual decarbonisation continue to underpin Singapore's marine and offshore demand, while the operating environment continues to be shaped by geopolitical uncertainty, capital expenditure discipline, pricing pressure, and cost volatility. In this context, BH Global Corporation Ltd ("the Group") experienced competitive price pressures in the current financial year and expect this price pressure to continue into the new financial year and will remain focused on operational resilience, margin discipline, revenue diversification, and alignment with Singapore's maritime transformation initiatives.

Singapore Marine & Offshore Market Conditions

Singapore continues to be a leading maritime and offshore hub, supported by established shipyards, offshore engineering capabilities, and a stable regulatory framework. Activity levels are expected to reflect disciplined capital spending, with maintenance, repair, and compliancedriven retrofit works providing baseline demand, while large discretionary projects may be phased, delayed or competitively tendered. The Group is prioritising projects within the Global shipyards and ship supply ecosystem where demand is operationally essential or compliancedriven, focusing on project selectivity and execution efficiency rather than aggressive volume growth.

Offshore & Energy Developments

Global upstream investment in offshore energy remains stable but selective. Demand for offshore support vessels, floating production storage and offloading units, and life-extension works is expected to remain measured. BH Global is strengthening its technical and engineering capabilities in system integration and upgrades. The Group aims to maintain closer engagement with shipyards and contractors to secure recurring supply arrangements. The renewable and offshore wind segment in the Asia-Pacific continues to develop gradually. While near-term visibility remains moderate, the Group continues to position its electrical and energy-related product offerings to support hybrid and energy-efficient marine applications should project momentum increase.

Sustainability and Decarbonisation

Sustainability and decarbonisation remain key priorities for the industry. Singapore's Maritime and Port Authority continues to promote vessel electrification, alternative fuels, and energy efficiency initiatives, while IMO carbon intensity regulations are expected to drive incremental retrofit activity. The Group is expanding its capabilities in vessel electrification and energy storage, promoting energy-efficient LED retrofits, and enhancing digital power management systems. These initiatives are focused on practical, commercially viable and compliance-driven solutions.

Digitalisation and Cybersecurity

Digitalisation and cybersecurity continue to advance across Singapore's maritime ecosystem, with smart port initiatives, predictive maintenance integration, and inventory digitisation becoming increasingly important. BH Global is strengthening its Cyber Security Division's capabilities to meet rising maritime cyber risk compliance requirements. The Division provides practical, standards-aligned solutions that integrate seamlessly with existing marine systems, helping customers achieve operational efficiency. Its work spans across Maritime, Commercial and Governmental projects, reflecting the growing demand for compliance-driven, riskmitigating cybersecurity solutions.

Supply Chain and Cost Management

Global supply chains remain exposed to geopolitical disruptions, logistics uncertainties and component shortages. Raw material prices, particularly copper and electronic components, continue to fluctuate, contributing to cost volatility. In addition, tariffs affecting certain export markets have continued to increase cost pressures within the Group's LED Manufacturing operations.

The Group mitigates these risks through diversification of supplier networks, prudent inventory buffers, closely monitoring of currency and supplier pricing, and exercising disciplined pricing strategies to protect margins. Labour costs in Singapore remain elevated due to structural manpower constraints, prompting continued focus on productivity improvements, digital workflows, cross-training, and selective automation.

Competitive Landscape

Singapore's marine supply market remains competitive and price-sensitive, with customers prioritising reliability, lead-time certainty, compliance, and technical capability. Competitive intensity has increased amid slower project momentum, resulting in tighter margins across the sector. BH Global is deepening long-term relationships with shipyards and ship owners, strengthening its value proposition through bundled solutions and robust technical support. In the current environment, differentiation is achieved through execution reliability, service responsiveness, and regulatory alignment rather than price competition alone.

Strategic Priorities

Management remains cautious but constructive on the Singapore marine and offshore outlook. While growth acceleration may be moderate, the structural role of Singapore as a maritime hub and the regulatory-driven nature of much marine spending provide a stable operating base. The Group's emphasis remains on resilience, disciplined execution, and gradual capability enhancement to navigate an evolving but fundamentally stable industry landscape.